What’s a Community Bond, Anyway?

Leveraging the power of community for social impact.

Why It Matters

Thanks to ever-changing political environments and limiting restrictions imposed on nonprofits by funding bodies, the ability of non-profit organizations to grow and secure their long-term is often hampered. One solution? Community bonds present an opportunity for organizations to leverage the power of their community to fund projects that can have a big impact, even beyond real estate usefulness. Christopher Trotman of Tapestry Community Capital gives us a primer on the impact investing tool.

In January 2019, the Ontario government announced a $15 million reduction to the Ontario Trillium Fund, money that would have gone to fund dozens of community projects. In May 2019, it was announced that close to $60 million would be cut from provincial programs geared towards funding the arts and culture sector. This included the elimination of the Indigenous Culture Fund that was established only the year before, in 2018. Even during a period when reconciliation is such a large public focus, the decision to cut a recently established program was made.

Clearly, there is no guarantee of funding when relying on money coming from government programs. That inconsistency can make it hard for the impact sector to imagine: what would it look like if an organization had the sort of financial stability that would allow them to put programming first? If rather than planning on one- to three-year funding cycles, an organization’s funding sources were diverse enough to plan for the next five years, with confidence that revenue would keep up with those plans?

One innovative funding tool — community bonds — has already helped several organizations the province achieve that financial independence, and this tool is starting to gain popularity.

What are community bonds?

Community bonds are a debt financing tool issued by non-profit, charity, or co-operative organizations for the purpose of investing in a capital asset — such as a building purchase, major renovations project, or a major equipment purchase. Community investors purchase bonds and are paid interest for investing in a project that is meaningful to them, and in return, the issuing organization gains access to the capital they need to grow. The organization is then responsible for repaying the capital investment to their community of contributors at the end of the bond term.

Community bonds are probably best known for helping nonprofits secure real estate, helping them scale in an area in which they’ve already proven valuable. One of the most well-known examples of an organization leveraging community bonds for the significant growth of their programming is the Centre for Social Innovation (CSI) in Toronto.

In 2010, CSI launched their first community bond issuance, raising $2 million through a community of 58 citizen investors to purchase a building in Toronto’s Annex neighbourhood. In 2014, the organization did it again, raising $4.3 million through 227 community bond investors to help fund the purchase of 192 Spadina Avenue, asking funders for a minimum investment of $1,000. CSI continues to leverage the community of investors that was developed through the first bond raise to fund the continued growth of their organization.

But organizations have used community bonds for more than real estate purchases. ZooShare, a bio-gas plant co-op which plans to recycle local food waste and manure from the Toronto Zoo to create renewable power for the Ontario grid, raised over $1.1 million in community bonds on their road to launch. Calgary-based Windmill MicroLending, which helps skilled immigrants and refugees further their careers in Canada by providing them with micro-loans for Canadian accreditation and training, has also leveraged community bonds as a funding base to expand their own lending pool. Montreal’s Le Grand Costumier, a social enterprise dedicated to managing costumes for Canada’s creative community, has used community bonds to restore and revitalize a costume collection received from Radio-Canada.

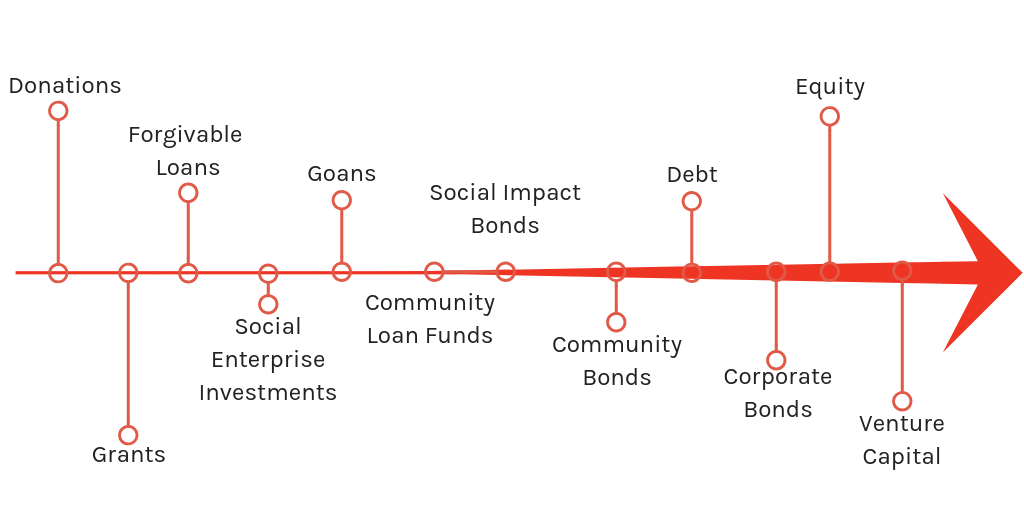

Where do community bonds fit within the social funding ecosystem?

Community bonds

Community bonds help not-for-profit organizations secure the long-term sustainability that can be found through ownership of a community asset, such as property or equipment. Bonds are ideal for capital development projects that have a significant community impact over the long-term, with a plan in place to repay funders (with interest).

Community bonds are not designed to fund the ongoing operational and programming costs of an organization, as they need to provide a return for investors. In addition, there are capital requirements for conducting a community bond campaign, and organizations need funding sources outside of the community bond to leverage the tool appropriately: the have to fund a marketing campaign to effectively reach out to their stakeholders, pay a lawyer to deal with legal documents, maintain ongoing communication with bond holders throughout, and set up infrastructure for the long-term management of the bond (from interest calculation and disbursements to management reporting).

Investors can also be effectively reengaged for future campaigns. For small projects under $500,000 or for funding the ongoing costs for an organization, a bond campaign would not be ideal due to the costs and effort involved.

Investment continuum graphic by Tapestry Community Capital.

Grants & funding

Grants are a cornerstone of most non-profit organization funding framework. Grants are non-repayable funds distributed by one party (often governments, foundations or corporations), to a recipient that may or may not be a not-for-profit organization. Most grants are earmarked for a specific type of project, either serving a particular community or involving a predetermined set of outcomes. Grants typically require some level of reporting to account for how the funds were used.

Part of the reason why grants are so valuable to not-for-profit organizations is that it is a relatively low-cost way of securing significant dollars to fund operational costs. The major cost of applying for a grant is time, as there are typically application processes that, in some cases, can be multi-layered. However, once the funds are granted, they do not need to be repaid, so there is a significant incentive to invest that time.

The major disadvantage of grants is they are not guaranteed year over year. At any point, a granting body can either change the requirements for the grant, or cut the grant completely. This can potentially leave an organization that has relied solely on grants or government funding in a precarious situation. Additionally, grants are always earmarked for a specific purpose, and they typically target programs that directly impact a target population. This sort of inflexibility means that organizations may not have funds where they are needed most, whether that’s marketing costs, technology upgrades, or major capital campaigns.

Fundraising & donations

Fundraising for a good cause is a practice that is as old as human civilization. Fundraising represents a direct appeal to a community of supporters for voluntary donations towards a cause or campaign. For non-profits of all sizes, fundraising represents at least some percentage of the organization’s funding base.

An experienced fundraising team can turn charitable giving into a significant part of a non-profit’s funding base. These are unrestricted funds that can be directed towards any cause of significant need for an organization with no additional reporting requirements. When done effectively, fundraisers can see an average return of $1.00 for every $0.24 spent of fundraising activities.

For smaller organizations that don’t have a history of appealing for large capital projects, fundraising may not be the most effective tool. Donors have fairly predictable funding habits, and unless there is a very strong appeal made, it can be difficult to galvanize supporters to give more.

As a source of ongoing predictable funding, an annual fundraising strategy can provide a stable part of an organization’s funding base. However, for large capital campaigns far outside of the typical funding habits of a community of supporters, fundraising alone may not be sufficient.

Crowdfunding

While some form of crowdfunding has been in practice since the 1700s, it’s generally agreed that the modern iteration of crowdfunding started in 1976 with British rock band Marillon. The band raised $60,000 to travel to the United States entirely through online fan donations. It wasn’t until years later, in 2009, that one of the most well-known crowdfunding platforms, Kickstarter, was founded.

Crowdfunding comes in a variety of forms including reward-based, equity-based, donation-based, and debt-based. The advantage of crowdfunding is that it is largely driven by social media marketing, making the upfront costs for a campaign potentially very low. The money can be raised for any purpose and depending on the nature of the campaign, there may be no need to pay those funds back.

The disadvantage of crowdfunding is that it typically provides very little security for the investor. With a general absence of reporting requirements, if an organization does not fulfill on their commitment, or uses the funds in a way that was not advertised, there is little recourse for the investor. In addition, the amount of money that a not-for-profit can expect from a successful campaign is fairly low. For a donation-based campaign, the average donation size is $66 and the average amount raised is $9,237.

Crowdfunding should not be relied on for a capital campaign or the ongoing operational costs of an organization. Rather, this tool is best reserved for smaller, one-time purchases between $5,000 and $25,000. Larger campaigns are possible, but they’re not the norm, and with an average success rate of only 36 percent for a fundraising campaign, it may not be worth the effort.

Social impact bonds

In some ways, social impact bonds are similar to community bonds, because they’re issued by community-focused nonprofits and charities. They too, create impact investment opportunities for individuals who believe in the mission of the issuing organization.

The main difference, however, is that in social impact bonds, the issuing organization has established an agreement with the government, where the government will pay for performance by the nonprofit or charity. The payment from the government is tied to clear social or environmental outcomes to which the issuing organization has committed, and these government funds are used to repay investors. So rather than investing in the business model of a social enterprise or revenue-generating nonprofit (as is the case for community bonds), investors in SIBs are investing in the organization’s ability to realize detailed social or environmental outcomes.

Social impact bonds can help charities that don’t have a revenue-focused repayment model, but they’re also held to clear — and sometimes limiting — targets for their results. The investors targeted for SIBs are often high net worth, accredited investors, while community bonds enable people of average means to transform from occasional donors or volunteers into citizen investors.

Selecting the right tool for the job

While community bonds are an amazing addition to the toolbox available to non-profit organizations, they are still just another tool. They provide an opportunity to build a strong foundation through the ownership of community assets. However, like any tool, community bonds are purpose-built, and should be used in combination with all of the funding mechanisms available to an organization.

In this way, organizations can really get to work on impacting the communities they were created to serve.

Your job. Your mission. Your news.

With your support, the sector you're building gets the journalism it deserves, and you get a tax receipt.

Related Articles

Case Study: Kingston’s food bank pilot combines three innovative solutions for food insecurity

Carney’s National Food Strategy includes boosting local food production. Pilots are already deployed. The federal strategy is arriving to meet it, not lead it.

How foundations responded to the 2004-2005 disbursement quota reduction – and why it matters now

Research from Carleton University, based on foundations’ T3010 data between 2000 and 2017, tells a story of how foundations adjusted their disbursements when the disbursement quota was reduced from 4.5 per cent to 3.5 per cent.

Explainer: What Realize Fund I’s final close says about the state of Canada’s social finance

Ottawa bet $400 million that public capital could build a private market for Canada’s social economy. Realize Fund I’s $276.7M close is the first real test.