Explainer: What Realize Fund I’s final close says about the state of Canada’s social finance

Ottawa bet $400 million that public capital could build a private market for Canada’s social economy. Realize Fund I’s $276.7M close is the first real test.

Why It Matters

Realize Fund I's close proves the federal wholesaler model can pull in roughly two private dollars for every public one — but the fact that 17 of its 23 backed fund managers are first-timers shows how thin and recent this credibility infrastructure still is. The real reckoning comes after 2030, when public anchor money disappears, and the sector finds out whether it built a durable market or just rented one.

This month, Realize Capital Partners, one of the three federal wholesalers of Canada’s Social Finance Fund, announced the final close of Realize Fund I at $276.7 million.

For most Canadians working in the social sector, that sentence may feel distant from daily reality. However, the hidden mechanics show how federal money is being used — not just to solve social problems directly, but to build an entirely new financial ecosystem capable of channelling far more capital toward them.

@futureofgood Big milestone🎉 One of three federal wholesalers of Canada’s social finance fund announced the final close of its fund. #nonprofitsoftikok #socialfinance #impactinvesting #Canada #nonprofits ♬ original sound – Future of Good

Realize Fund 1 is part of a system designed to move money to co-operatives, non-profits, social enterprises, and community loan funds that conventional capital markets have long passed over.

It is what market-building actually looks like in practice.

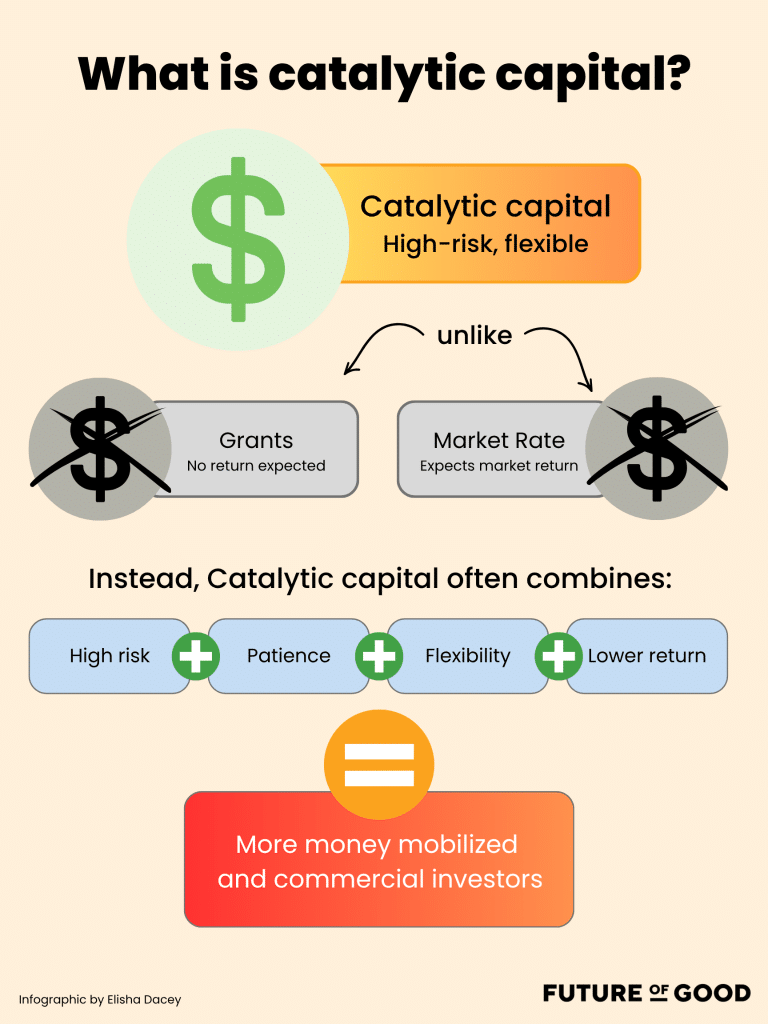

The 2-for-1 multiplier effect

The Social Finance Fund (SFF) was created to address the vast, largely unmet demand for financing among social purpose organizations — co-operatives, non-profits, social enterprises, community loan funds — that conventional capital markets, like banks, don’t serve well.

It relies on the growing pool of investors interested in generating returns alongside measurable social or environmental impact.

The SFF is what practitioners call catalytic capital: public money that accepts lower returns than a conventional investor would demand, precisely so that other, more commercially minded investors feel safe coming in.

The federal government committed $755 million to the SFF. Of that, $400 million was invested directly in three wholesalers, with the expectation that they would match it with private capital.

The overall target is to grow that public investment to more than $2 billion in total social investment — roughly two dollars of private capital for every public dollar deployed.

Ottawa selected three wholesalers — Realize Capital Partners, Boann Social Impact, and Fonds de finance sociale – CAP Finance — and divided the $400 million among them, each with a mandate to attract additional private investment.

Each wholesaler operates in a specific region: CAP Finance is dedicated to Quebec’s ecosystem; Realize and Boann cover the rest of Canada.

The singling out of Quebec is important. CAP Finance reflects Quebec’s longer, more developed tradition of solidarity finance — a model of community-rooted investing that predates the SFF by decades and includes major institutions like the Fonds de solidarité FTQ and Fondaction CSN, among others. (Solidarity finance, for those unfamiliar, is a Quebec term for a cooperative, values-based approach to investment that prioritizes community benefit alongside financial return — distinct from but related to the broader concept of social finance.)

When CAP Finance announced its first investments — including in BKR Capital and Theia Partners — it was building on decades of institutional groundwork.

The $90 million CAP Finance received from the SFF, combined with private partners including the Fondation Lucie et André Chagnon, is expected to attract close to $200 million in additional private investment in Quebec alone.

What is a ‘fund of funds’, and why is it a relevant solution

Realize Capital Partners chose to build a fund of funds — a structure that, rather than investing directly in individual companies or projects, invests in other funds. Those funds, in turn, deploy capital into social purpose organizations.

Think of it as a portfolio of portfolios: instead of picking individual investments, the fund-of-funds gains exposure to a curated set of fund managers, each with their own expertise, geography, and impact focus.

The structure pools resources, spreads risk across asset classes — private equity, private credit, real estate, venture capital — and transfers the demanding work of evaluating dozens of managers to a specialized team with both financial and impact expertise.

For an investor — whether a university endowment, a community foundation, or a bank — who wants exposure to impact investing but lacks the in-house staff to simultaneously evaluate, say, a microlending fund in Halifax, an Indigenous affordable housing fund in northern Saskatchewan, and a cleantech fund in Vancouver, the fund-of-funds offers a single entry point.

The investors who pool capital in a fund of funds (known as limited partners, or LPs — their liability is limited to the amount they’ve committed) gain exposure to all 24 investments in Realize Fund I’s portfolio without having to individually assess each one. What they’re buying, in effect, is expertise and access.

Concordia University’s Inter-Generational Fund committed $25 million to Realize Fund I, making it one of the fund’s anchor investors. Its Chief Investment Officer, Marc Gauthier, describes the impact fund-of-funds as a solution to a genuine, practical problem: “The breadth of impact investment opportunities in the Canadian market means it’s hard for a new team to know where to start.”

The UK’s Better Society Capital pioneered this wholesaler-plus-fund-of-funds model, launched in 2012 under a similar blended finance mandate. By the end of 2024, the UK social impact investment market it helped build had grown to £11.2 billion (about $21 billion) — a 12-fold increase in 12 years.

Canada is watching, and borrowing.

The 17-out-of-23 statistic that matters most

While this financial architecture is interesting, what it produces may be more so.

Of the 23 fund managers Realize has backed so far, 17 are new or emerging organizations that would have struggled to raise institutional capital without the credibility signal of a major anchor investor.

Of Realize Fund I’s 32 LPs, more than two-thirds are investing in social finance for the first time.

This is what market-building actually looks like: not a single transformative investment, but the patient, unglamorous work of giving first-time fund managers their first institutional vote of confidence, so that other investors follow.

Misfit Ventures, Canada’s first LGBTQ+-focused venture capital fund and a Realize investee, put it plainly.

“As a first-time fund manager, one of the biggest challenges is building early credibility in a space where institutional capital has historically been slow to back underrepresented managers.”

Boann Social Impact, another SFF wholesaler, has committed nearly $51 million across 13 impact funds — including the Raven Indigenous Outcomes Funds, which addresses diabetes prevention and housing electrification in Indigenous communities through outcomes-based financing.

Like Realize, Boann has deliberately built its portfolio around first-time, emerging, and established managers, with particular attention to underserved regions: Northern, Atlantic, and the prairies.

Flowing River Capital Partners, an Alberta-based, Indigenous-owned fund backed by Realize and investing primarily in prairie companies, is a clear example of who the wholesaler model was designed to serve: mission-aligned, geographically focused, and deeply rooted in the communities it serves — but historically cut off from institutional capital.

What impact investors are actually funding

Taken together, the portfolios built by Realize and Boann sketch a picture of what Canada’s social economy looks like when it receives capital.

Realize Fund I includes: a private credit housing fund building affordable homes in Indigenous communities; a microlending fund supporting foreign-educated professionals locked out of employment commensurate with their credentials; a cleantech private equity fund investing in commercially ready solutions that decarbonize the power supply and electrify transportation; and a health-focused venture capital fund targeting cancer therapies.

Boann’s investees include a fund financing outcomes contracts for Type 2 diabetes reduction in Indigenous communities, and three Vancouver-based cleantech venture capital funds.

A March 2026 report from the Institute for Sustainable Finance and Rally Assets offers the clearest picture yet of how quickly this market has grown.

Canada’s private impact investing market now stands at $17.7 billion in cumulative target capital — money that fund managers have set out to raise, not necessarily capital already deployed.

Annual target capital has increased nearly ninefold since 2021, and product launches hit a record 55 in 2025 — a sevenfold increase from the same baseline — with almost half launched by first-time fund managers.

That is significant growth.

But the same report notes it has been uneven: venture capital has dominated, geographic representation outside Ontario and B.C. remains limited, and asset owner allocations to impact investing are still modest compared to the scale of the problems being addressed. Growing a market is not the same as solving the underlying challenges.

Honest tensions

The following concerns arise from the ISF/Rally Assets market report, academic research on the SFF’s design, and the federal government’s own acknowledgment of impact measurement gaps.

First is the transmission problem. There is a structural risk in any layered investment model: each intermediary layer entails costs, management fees, and return expectations. A social purpose organization at the end of this chain — the housing co-op that eventually receives a loan from a community fund that received capital from a wholesaler — is several steps removed from the original public investment. Whether the terms remain affordable and the impact rigorous at each step is a question the sector is actively working through.

The SFF’s decision to begin requiring Social Equity Lens Investment (SELI) reporting in 2026 is a direct response to this concern.

{kind=link}

Next is the limits of leverage as a metric. The 2:1 ratio is a compelling headline, but it can paper over a real tension: private capital comes with its own expectations around returns, time horizons, and risk tolerance, which don’t always align with the most underserved communities or the most intractable problems.

The Ronald S. Roadburg Foundation, a Realize Fund I LP, described the fund’s ‘diversified and de-risked structure’ as a ‘no-brainer’ — and that is precisely its appeal to many investors. But it also explains why the most structurally difficult investments remain harder to reach, even within the impact market.

The last is the public subsidy question. The market-building approach assumes that once the scaffolding is in place — the intermediaries, track records, and investor education being built right now — private capital will continue flowing without ongoing public support. This is the SFF’s core bet over its 10-year horizon. The UK experience offers cautious optimism: markets can be built. But they also need sustained support, especially where margins are thinnest, and impact is deepest. As of December 2024 — before Realize Fund I’s final close — the SFF had already helped leverage over $322 million in private capital across all three wholesalers.

The real test comes after 2030, when public anchor investment is withdrawn.

A Blueprint, With Caveats

Realize Fund I’s final close is a milestone worth pausing on.

At $276.7 million, it is large by any Canadian standard — the typical impact fund in this country closes between $10 million and $100 million — and the fact that it closed at all in a difficult fundraising environment for private markets generally is significant in its own right.

Realize Fund I’s initial target was $405 million. Realize team pitch to 500 investors before landing on 32.

The 32 LPs who participated — including Royal Bank of Canada, the McConnell Foundation, the Trottier Family Foundation, the Saskatchewan Community Foundation, the Toronto Foundation, and Concordia University — represent a notable broadening of who is willing to call themselves an impact investor.

Kelly Gauthier, President of Realize Capital Partners, has described the fund as a potential blueprint — proof that government capital can be used to bring private investment into community-benefiting enterprises that would otherwise not attract it.

The harder question remains open: whether this architecture will ultimately reach the social purpose organizations that most need flexible, patient capital, in the communities most underserved by conventional finance.

The wholesalers have until 2030 to demonstrate that they can.

The measurement frameworks are still taking shape.

First-time fund managers are still building their track records. Community foundations, university endowments, and philanthropic organizations that are committed to Realize Fund I are, in many cases, still learning what impact investing means for institutions with fiduciary duties and decades of conventional practice.

What is already clear is that something real is being built — carefully, deliberately, with more public money and private intent than Canada has ever directed at this problem before.

Whether it reaches the right places is the story that has only just begun.

Your job. Your mission. Your news.

With your support, the sector you're building gets the journalism it deserves, and you get a tax receipt.

Author

Related Articles

Case Study: Kingston’s food bank pilot combines three innovative solutions for food insecurity

Carney’s National Food Strategy includes boosting local food production. Pilots are already deployed. The federal strategy is arriving to meet it, not lead it.

How foundations responded to the 2004-2005 disbursement quota reduction – and why it matters now

Research from Carleton University, based on foundations’ T3010 data between 2000 and 2017, tells a story of how foundations adjusted their disbursements when the disbursement quota was reduced from 4.5 per cent to 3.5 per cent.

Inspirit Foundation’s 100% impact portfolio outperforms benchmark over 10-year period

Inspirit Foundation became the only Canadian foundation to successfully transition 100 per cent of its assets to impact investment in 2022. Since the foundation first made the commitment in 2016, its portfolio has made higher returns than a traditional portfolio would.