Quebec asset manager makes unique investment, draws attention to benefits of community bonds

Perception isn’t reality. Experts share how community bonds offer sound returns.

Why It Matters

Community bonds campaigns don't attract big private or institutional investors, but Addenda Capital's first investment might change that.

Carl Pelland is VP of Fixed Income and Head of Corporate and Impact Bonds at Addenda Capital. Gabriel Tremblay is CEO of social economy enterprise TAQ Group. Réjean Nguyen is Senior Director of Impact Investing and ESG Integration at Addenda Capital. Alexandre Zarbatany is Director, Client Partnership and Business Development at Addenda Capital (Supplied photo)

Last month, Quebec-based asset manager Addenda Capital made a first-of-its-kind investment.

It purchased ten per cent of TAQ Group’s five million community bonds, a move that’s expected to generate returns while supporting a social economy manufacturing enterprise that employs people with disabilities.

Carl Pelland, Addenda’s vice-president of fixed income and head of corporate and impact bonds, said asset managers have not traditionally added community bonds to their portfolios.

And even if they did, the investment threshold was too small for an asset manager’s portfolio.

“We look for an investment of at least $250,000, and we do not want to make more than 10 per cent of the total amount,” Pelland said.

Rina Marchand, Groupe TAQ Impact investment manager, explained the rationale behind that.

Although there have been dozens of community bond campaigns across Canada over the last 15 years, most were relatively small. The average campaign was under one million dollars, she said.

Therefore, asset managers did not hear of these campaigns. Marchand said community bonds are becoming popular, but haven’t gone mainstream yet.

How TAQ designed its issuance to attract major investors

Réjean Nguyen, senior director of impact investing and ESG integration at Addenda Capital, said TAQ was the perfect opportunity for Addenda to explore community bonds.

The social enterprise designed its campaign to appeal to investors like Addenda.

“We created four series with different returns and investment thresholds,” said Marchand.

Addenda bought the first series. Designed with foundations and institutional investors in mind, it promises a five per cent return on five-year term investments.. It’s also the only series with annual interest.

Rina Marchand is an impact investment manager at TAQ Group. (Credit: Sylviane Robini)

The second series targets entrepreneurs, offering a four per cent return with a three-year term.

Series three and four are public; anyone wanting to invest in a community project can purchase them. The first offers a three-and-a-half cent return and a five-year term, and the latter offers no return and a three-year investment period.

Marchand said scenario-building was used to assess TAQ’s ability to repay its community bonds.

“With community bonds, you have to consider that some investors will reinvest when the term has expired, giving us access to new capital. Others will cash them in. And some will turn them into donations,” she said.

Community bonds or loans?

The idea of organizing a community bond campaign instead of soliciting another bank loan was first raised with TAQ’s board in 2024, said CEO Gabriel Tremblay, noting TAQ’s solid financial situation, which includes owning brick-and-mortar assets, made them eligible for traditional bank loans.

However, he believes a community campaign offers greater benefits than a bank loan for a mature and reputable non-profit like TAQ.

“Instead of having three financial partners, we will have 200,” Tremblay said.

“That is 200 persons who will receive information about our job creation, new contracts, and how we change lives. It is a long-term initiative.”

The argument resonated with the TAQ board, which authorized a five-million-dollar campaign that could be raised to 10 million in the future.

TAQ then worked with Le Fonds l’Ampli to develop an issuance structure. L’Ampli is a fund that also offers support. Analysts assist non-profits like TAQ in structuring their community bonds campaign. L’Ampli also assists cooperatives in issuing shares.

In both cases, an organization may receive up to $100,000 in loans to finance the issuance.

“I reviewed the TAQ dossier for l’Ampli and recommended a $100,000 loan to help cover their campaign costs,” said Alexis Grégoire-Gendron, financial analyst for Réseau d’investissement social du Québec (RISQ), the organization responsible for conducting financial due diligence on social economy projects.

Grégoire-Gendron’s analysis helped give Addenda the confidence it needed to make its first community bond purchase.

Alexis Grégoire-Gendron is financial analyst at Réseau d’investissement social du Québec (RISQ) (Supplied photo)

“I showed Addenda’s team how to evaluate a social economy enterprise beyond financial metrics. I pointed out what to look for in the TAQ dossier,” he said.

Community ties are a good indicator of a social enterprise’s soundness, Grégoire-Gendron said.

“Community ties are made of the number of volunteers, the government support through programs or procurement policies, the belonging to groups, etc. It shows how rooted you are in the community,” he said.

Addenda will add $500,000 TAQ community bonds to its $700 million Impact Fixed Income Fund, a bond-only fund launched in 2018.

“We select impact bonds offering a financial return aligned with regular Canadian bonds, plus a social or environmental return,” Pelland said.

Nguyen said Addenda’s impact fund appeals to foundations, religious communities, and some insurance companies. It covers five themes: climate change, health and wellness education, water and community development.

The quest for local social impact

Climate-related bonds make up two-thirds of the fund’s offering.

“Diversification into social impact, especially local impact, has been at the top of our minds since the beginning,” said Nguyen.

However, Pelland said these types of investments are difficult to find, and social impact metrics are challenging. Investors are more comfortable with efficiency and renewable energy projects.

Addenda has been exploring community bonds for a while, but struggled to find a suitable solution. That changed in 2025.

TAQ fits into the community development category Pelland was searching for, as do First Nations Finance Authority bonds. The authority is a not-for-profit that provides qualifying First Nations with venture capital.

The Indigenous organization issues bonds once or twice a year, said Nguyen.

“Investors like us get informed yearly about the specific projects their issuance finances. It could be water sanitation, affordable housing, etc.,” he said.

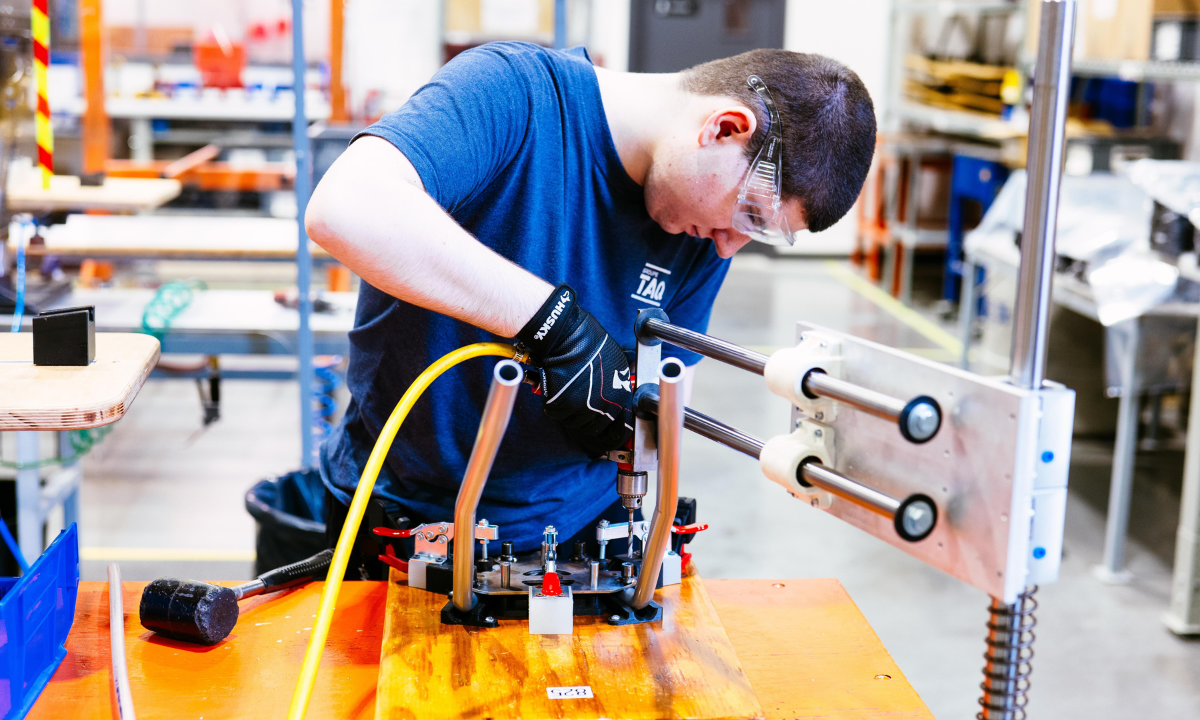

TAQ Group is a manufacturing company employing people with disabilities. (Supplied photo)

Pelland said detailed reporting is essential for impact investors. TAQ will hold quarterly calls with Addenda to provide progress reports about its activities.

Such calls are mandatory for publicly listed companies so financial analysts can inform investors about the status of their investments.

Grégoire-Gendron said TAQ calls create a ripple effect.

“It will contribute to Addenda’s understanding of the social economy sector. They might share their knowledge with other asset managers, raising interest for future major community bonds campaigns,” he said.

“Our first meeting was very Cartesian,” said Tremblay.

“These guys are used to buying corporate bonds. We explained that TAQ generates revenues and surplus, just like a corporation. But our return will never be 30 per cent, and it will not be redistributed. We reinvest everything to serve the mission, hiring more persons with disabilities,” he said.

That approach suits Pelland.

“When TAQ contacted us, some of our impact investors had already dropped a line about their upcoming issuance. They wanted us to take a look,” he said.

Impact investors want to invest locally. Community bonds give them this opportunity, added Nguyen.

Exception or opportunity?

Grégoire-Gendron said Addenda’s investment could mark a pivotal moment in the development of the community bond ecosystem.

“However, let’s remember that these bonds are a community tool. Its strength lies in the popular support. Social economy enterprises can design series for asset managers and institutional investors. But it should not be their primary focus, otherwise community bonds will weaken their essence,” he said.

Tremblay sees this as a turning point.

“Until now, investors had no idea how to fit community bonds into their investment strategy,” he said.

While preparing its campaign, TAQ approached Quebec’s three tax-advantaged funds: Fondaction, Fonds de solidarité, and Capital régional Desjardins. They were not interested.

“Now that a private fund did it, they are ready to meet with us,” said Tremblay.

However, there are still barriers to overcome, including the perception that community bonds offer low returns.

“Not all the investments of those three funds exceed a five per cent return. So why not diversify 0.5 per cent of their portfolio with community bonds yielding three to five per cent?” added Tremblay.

The same goes for pension funds, he said. Montreal’s workers’ pension fund could invest 0.5 per cent into community bonds issued by the City’s social economy enterprises.

“Any Canadian city pension fund could do it,” he added

Marchand also pointed to an untapped pool of philanthropic capital: foundations looking to increase their endowment’s impact investments.

Between 2010 and 2024, Canadian philanthropic capital, the total amount available for philanthropy, increased by 285 per cent, said Karel Mayrand, CEO of Fondation du Grand Montreal, while speaking at a recent event in Montreal.

“However, during that period, donations increased only by 36 per cent,” said Marchand.

“Maybe a social enterprise does not fit into a foundation’s mission for a donation. However, all social enterprises fit the impact investment broad thesis. Again, 0.5 per cent of the philanthropic capital could be invested into community bonds,” she said.

Pelland said the size of the issuances, which bigger foundations, asset managers, and institutional investors will consider, may be the most significant barrier to investing in community bonds.

Group issuance could be the solution, suggested Nguyen.

“Imagine a Montreal, Toronto, or Vancouver Community Bonds Group. It would gather various campaign sizes to offer institutional investors the scale they need to invest. The group could be geography (city, region) or theme ( housing, community, energy, etc.),” he said.

Group issuance allows for blended finance, including products with different levels of risk and returns, attracting diverse investors.

This investment is the story of two parallel universes meeting, said Nguyen.

“There’s potential to develop others like this with different partners,” Pelland said.

“There are bridges to be built that could benefit both. TAQ and I have already spent many hours together and will spend more time together. We want to participate in developing this form of investment,” he said.

Your job. Your mission. Your news.

With your support, the sector you're building gets the journalism it deserves, and you get a tax receipt.

Author

Related Articles

Fundraising for Prime Minister’s residence renos called unusual, a ‘misstep’: Charitable advocates

Prime Minister Mark Carney announces competition, fundraising effort for 24 Sussex Drive

Canada improved its ‘poverty grade’, but Manitoba advocates say grading system needs improvement

Food Banks Canada released its annual poverty report card, where Canada received a slight boost in its grade. However, some advocates say the rating system has significant flaws.

How advocacy from the food bank sector led to the Canada Groceries and Essentials Benefit

While many in the sector have long campaigned for additional social assistance to address the rising cost of living, there is more to be done, they say. Now, they’re targeting a reform of Employment Insurance.