Why the world of impact should care about open banking

It sets the agenda for inclusive growth

Why It Matters

Open banking holds transformative potential to reduce costs, improve Canadians' ability to manage financial services, and gain access to a wider range of services. We haven’t yet had a significant conversation about the social purpose merits and potential of open banking. The time for that discussion is now.

In the past few weeks, two events quietly kicked off the next era of financial services in Canada: The Global Summit for Banking on Values and the Government of Canada’s consultations on open banking.

For the first time, experts from banking and fintech, policymaking, and consumer groups came together to explore what open banking means for growth, economic inequality, and consumer choice.

Although the events received little coverage, they have set in motion ideas and conversations that have the potential to catalyze a radically inclusive economy and society. So, pay attention.

THE BACKDROP

Banks have always held a wealth of data about their customers’ finances and habits. Over time, technology developments have made it easier to collect data, move it around, and make sense of it.

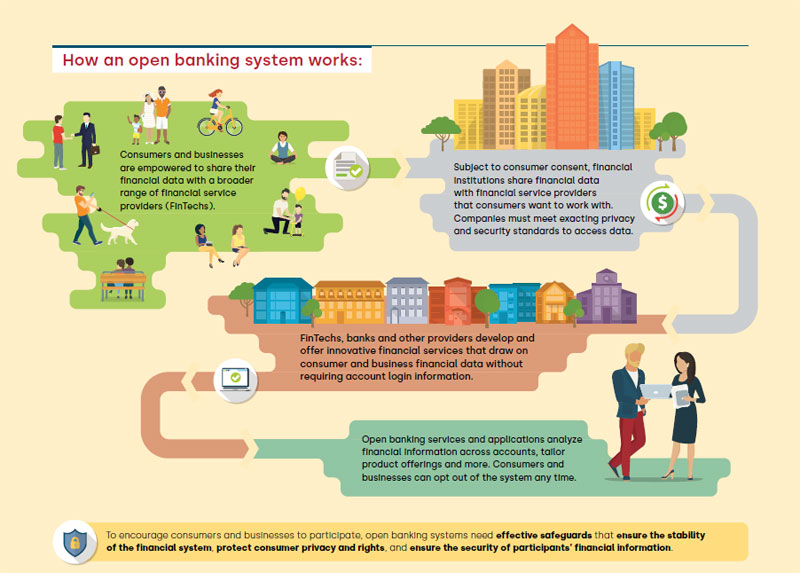

While carrying out banking activities, people generate a stream of data based on their transactions. This financial transaction data is currently held and controlled by individual financial institutions. Open banking changes this—for good.

You can think about open banking in the same way you might think about open data. It is where citizens can authorize third-party service providers to access their financial transaction data, using secure online channels. The benefit is that it allows them to access new products and services that can enhance their lives. However, these benefits aren’t assured. It’s possible that open banking can increase exclusion, inequality, and discrimination or become another data play industry.

WHAT WE SEE

Thus far, conversations on open banking have centred around how open banking could pave the way for the transformation of the financial sector to better serve consumers and grow businesses and markets, contributing to the growth of the Canadian economy and Canada’s global advantage.

We see numerous possibilities in the world of impact for open banking including apps that could analyze data to help humanitarian aid cash transfer, personal financial literacy and management, local economic development and entrepreneurship loan products, financial services tailored for gig workers, and newcomer settlement.

In order to deliver on these benefits, the finance system must have appropriate consumer protection, while also meeting standards with respect to privacy, security, and operational stability.

But first, as impact-focused people, we need to explore the merits of open banking for both our domain and the people we serve, as well as shape this emerging landscape. Organizations such as Prosper Canada have already begun, but its potential is broader than financial literacy and empowerment.

This is yet another window for the world of impact in Canada to lead the conversation for a more equal opportunity, low-energy, social procurement-based, and social enterprise-friendly industry.

(Aside: How do you think we fared on this with cannabis?)

WHAT TO WATCH

There are mixed perspectives surrounding what should be the primary policy and regulatory angle for Canada’s open banking system: Global competitiveness? Consumer choice? Inclusion? Something else?

Given the federal government’s emphasis on inclusive innovation and inclusive growth, particularly with the social innovation and social finance strategy, this focus on inclusion would be a worthwhile starting point.

Open banking can be a catalyst for inclusive innovation and lasting impact. We must not let it become another meaningless data play industry, but a multi-sector ecosystem that supports viable and purpose-first business models.

GO DEEPER

A Review into the Merits of Open Banking Government of Canada consultation document.

Your job. Your mission. Your news.

With your support, the sector you're building gets the journalism it deserves, and you get a tax receipt.

Author

Related Articles

Partnered Partnered content The dirt on cleaner farms: Regenerative agriculture reshaping Canada’s farming future

Farmers see higher profits and healthier soil when moving to regenerative practices, but face financial and policy barriers to making the transition.

Partnered Partnered content Les microcours ont pour but d’aider les Canadiens à acquérir des compétences professionnelles sans frais

Dans le cadre de l’ambition de RBC de doter les gens des aptitudes nécessaires pour réussir, nous aidons les Canadiens à s’adapter à l’évolution du marché du travail en leur offrant gratuitement des microcours et des outils de perfectionnement.

Partnered Partnered content Microcourses aim to help equip Canadians with job-ready skills at no cost

As part of RBC’s ambition to equip people with the skills for a thriving future, the financial institution is helping Canadians adapt to the changing job market with microcourses and upskilling tools at no cost.